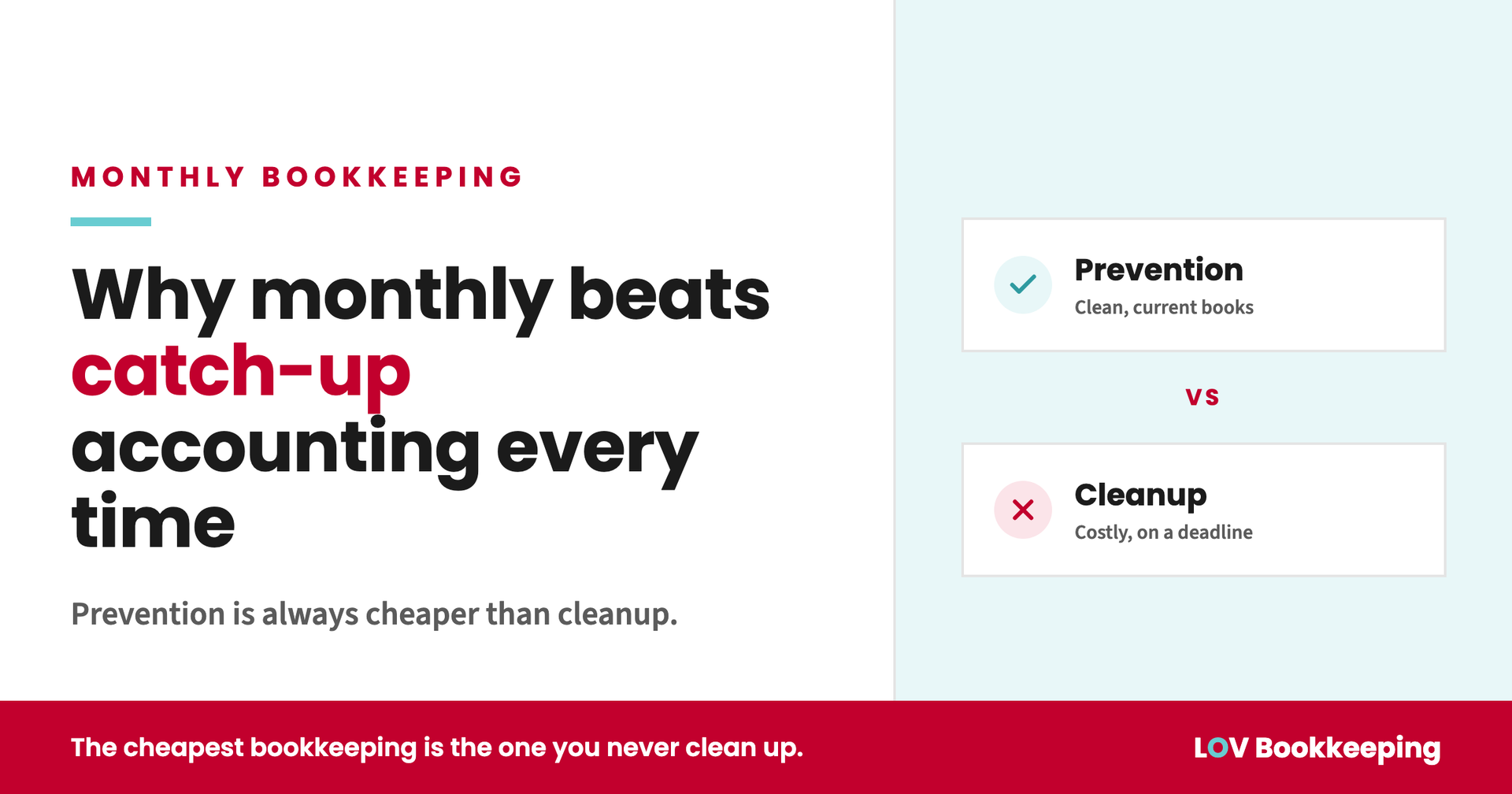

The Top 5 Bookkeeping Mistakes Small Businesses Make (and How to Avoid Them)

Bookkeeping is one of those behind-the-scenes tasks that can either support your business’s success or quietly undermine it. At LOV Bookkeeping, we’ve seen firsthand how small missteps in managing financial records can lead to major headaches. The good news? Most of these mistakes are entirely avoidable.

Here are the top five bookkeeping mistakes small businesses make—and how to steer clear of them.

1. Mixing Business and Personal Finances

This is one of the most common and damaging errors we see. Using the same bank account or credit card for both business and personal expenses makes it incredibly difficult to track true business performance, leads to inaccurate financial reporting, and complicates tax time.

How to Avoid It:

Open separate business checking and credit card accounts. Use them exclusively for business transactions. LOV Bookkeeping can help you set up a clean chart of accounts and ensure everything is tracked properly from day one.

2. Falling Behind on Recordkeeping

Bookkeeping isn’t a once-a-month task. Delaying data entry, expense categorization, or reconciliations can result in missed deductions, inaccurate financial reports, and cash flow surprises.

How to Avoid It:

Schedule time weekly (or outsource to a pro) to keep your records current. LOV Bookkeeping provides monthly services to ensure your books are always up to date and ready for decision-making or tax filing.

3. Misclassifying Transactions

Incorrectly categorizing income and expenses can distort your financial reports and may lead to issues with taxes or budgeting.

How to Avoid It:

Use a consistent and clear chart of accounts. If you’re unsure where something belongs, don’t guess—ask a professional. At LOV Bookkeeping, we build custom account structures that reflect your business accurately.

4. Ignoring Bank and Credit Card Reconciliations

Failing to reconcile your accounts regularly can leave unnoticed errors, duplicate transactions, or even fraud hidden in plain sight.

How to Avoid It:

Reconcile your accounts monthly to ensure all records are accurate and nothing slips through the cracks. It’s a standard part of our services at LOV Bookkeeping.

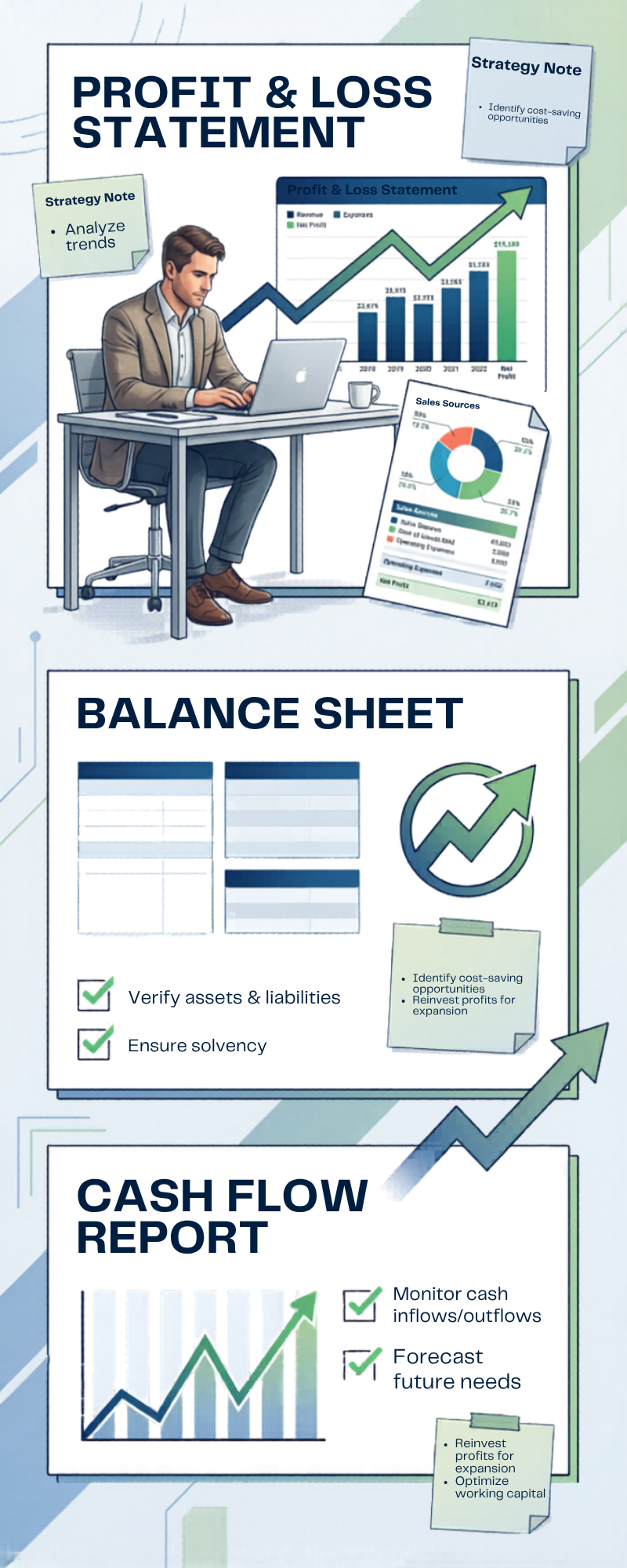

5. Not Reviewing Financial Reports

Many small business owners focus only on the bank balance, ignoring valuable reports like the profit & loss statement or balance sheet.

How to Avoid It:

Make reviewing your reports a regular habit. We go beyond data entry to help our clients understand what their numbers mean—turning data into insight that supports smarter decisions.

Conclusion

Mistakes happen—but when it comes to bookkeeping, a few missteps can cost your business time, money, and peace of mind. The good news? You don’t have to do it alone. At LOV Bookkeeping, we help small businesses stay organized, compliant, and ready for growth by avoiding these common errors before they become problems.

Let’s make sure your books are working for you—not against you. Contact LOV Bookkeeping to schedule your free consultation today.