Articles

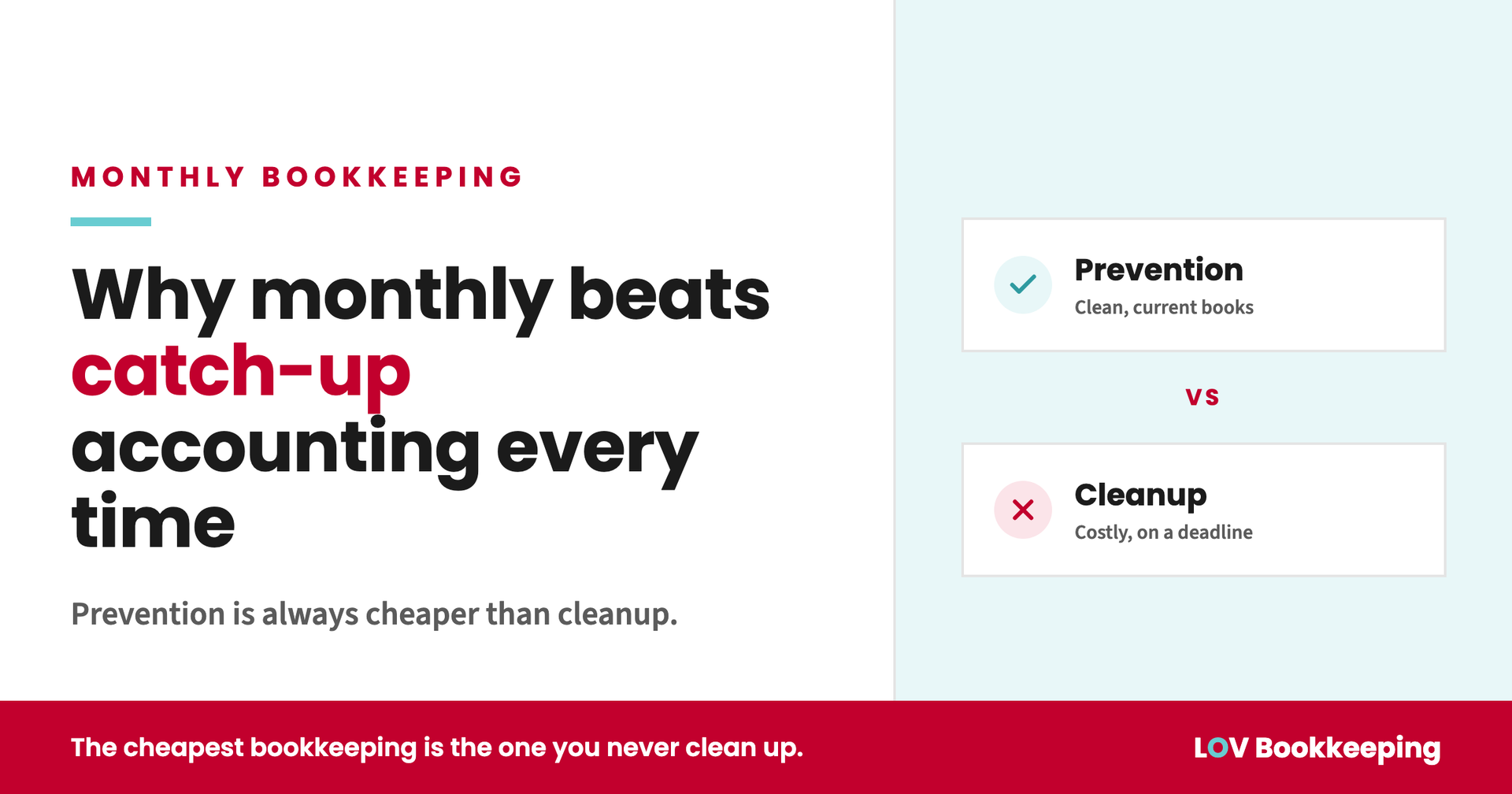

Most business owners we talk to assume catch-up bookkeeping is the budget-friendly choice. Let the books sit, hand off a pile of statements once or twice a year, and pay for a single cleanup instead of an ongoing service. On paper that sounds reasonable. In practice it usually costs more.

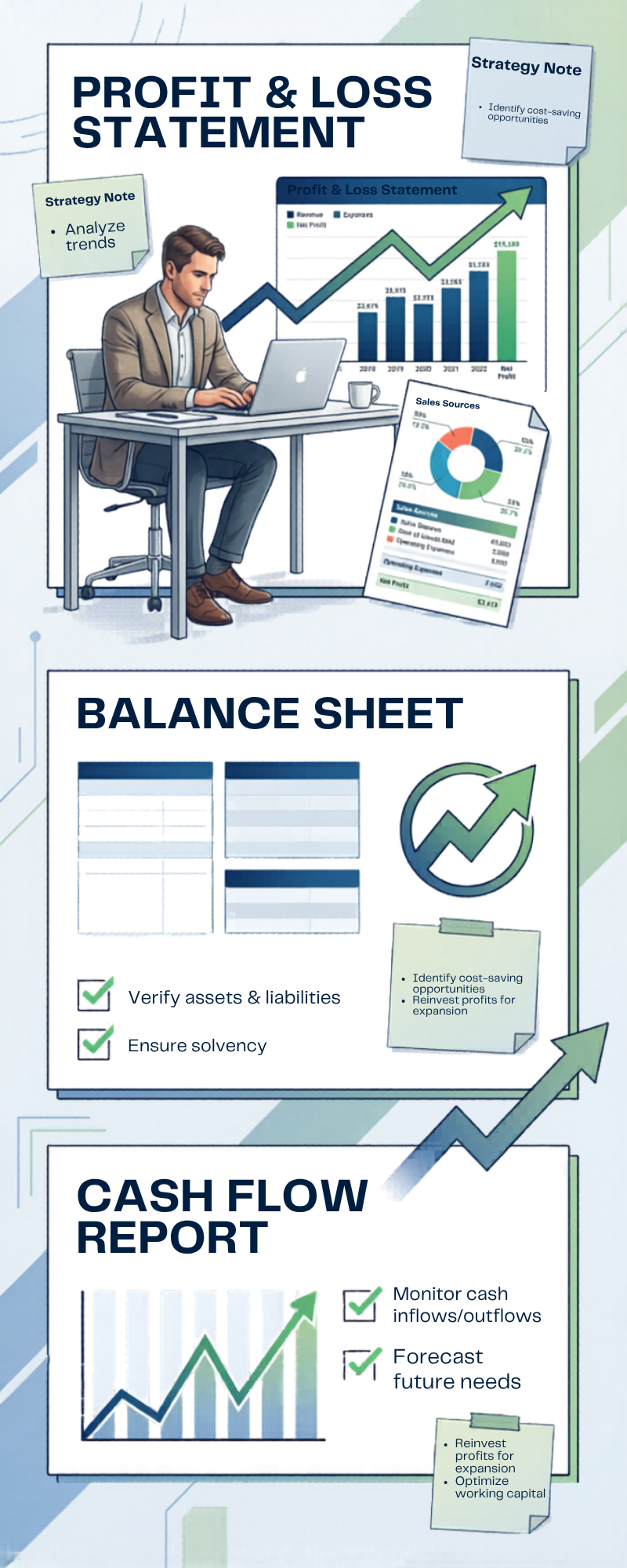

Many small business owners receive financial reports every month… but never really use them. The reports get downloaded, glanced at briefly, and filed away until tax season. But financial reports are much more than paperwork—they’re decision-making tools. When you understand what your numbers are telling you, you can make smarter, more confident choices for your business. Here’s how to turn your financial reports into actionable insights. Your Profit & Loss Statement Shows What’s Working Your Profit & Loss Statement (P&L) tracks: Revenue Expenses Profitability This report helps answer important questions like: Are you actually making money? Which services or products are most profitable? Are expenses increasing too quickly? Reviewing your P&L monthly helps you spot trends early instead of reacting after problems grow. Your Balance Sheet Reveals Financial Stability Your Balance Sheet gives you a snapshot of: What your business owns (assets) What it owes (liabilities) Your equity position This report helps you understand the overall financial health of your business. For example: Too much debt may signal risk Strong cash reserves create flexibility Growing assets often indicate stability and growth Cash Flow Tells You Whether Your Business Can Breathe Profit does not always equal cash in the bank. Your cash flow shows: Money coming in Money going out Whether you can comfortably cover expenses Many profitable businesses still struggle because they don’t monitor cash flow carefully. Understanding this report helps you avoid surprises and plan ahead with confidence. Financial Reports Help You Make Smarter Decisions When your reports are accurate and up to date, they help guide decisions like: Hiring employees Increasing prices Cutting unnecessary expenses Expanding services Investing in equipment or marketing Instead of relying on guesswork or emotions, you’re making decisions based on real data. Consistency Creates Clarity Financial reports only become useful when they’re reviewed consistently. Monthly bookkeeping and regular financial reviews allow you to: Spot problems early Track progress toward goals Make adjustments quickly Good financial habits lead to better long-term business decisions. How LOV Bookkeeping Helps At LOV Bookkeeping, we believe bookkeeping is about more than recording transactions. We help small business owners: Understand their financial reports Identify trends and opportunities Gain clarity about their business performance Make informed, confident decisions Because when you understand your numbers, you can lead your business with confidence.

For many small business owners, doing your own bookkeeping feels like the responsible thing to do. It saves money, keeps you in control, and seems manageable, at least at first. But what most business owners don’t realize is that DIY bookkeeping often comes with hidden costs. Over time, those costs can add up to far more than hiring a professional. Let’s take a closer look at the real cost of doing your own books.

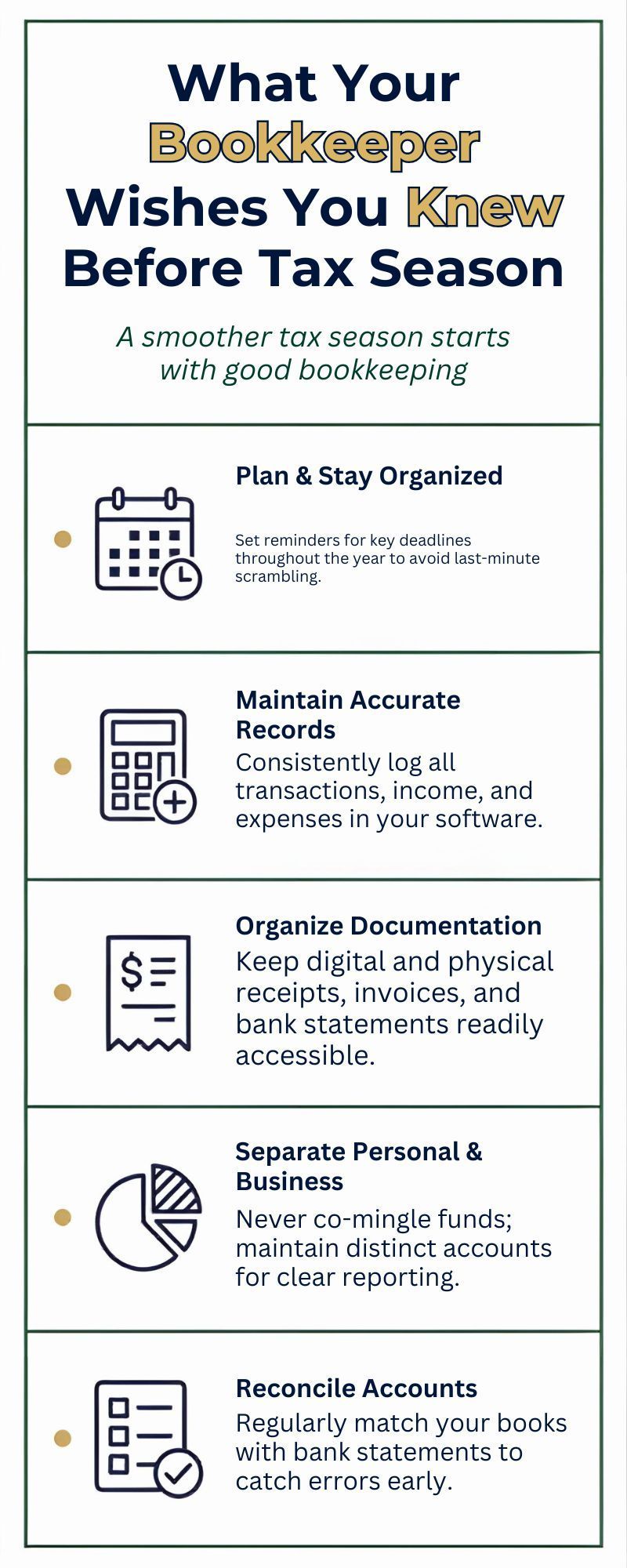

For many small business owners, tax season feels stressful, confusing, and rushed. Documents are being gathered at the last minute, questions pop up unexpectedly, and everyone is trying to meet deadlines. But the truth is, tax season doesn’t have to feel that way. A lot of the stress that happens in March and April could be avoided with better bookkeeping habits throughout the year. As bookkeepers, we see the same patterns every year, and there are a few things we wish every business owner understood before tax season arrives.

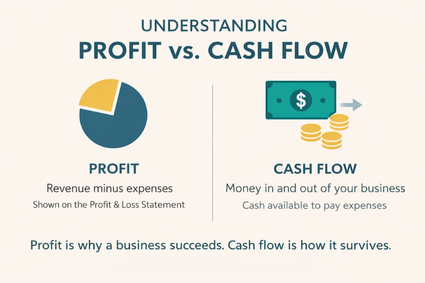

Many small business owners assume that if their company is profitable, they must be financially healthy. Unfortunately, that’s not always true. One of the most common financial misunderstandings is confusing profit with cash flow . While they are connected, they are not the same—and understanding the difference can protect your business from serious financial stress.

A new year is the perfect time for small business owners to reset, refocus, and build better financial habits. While motivation is high in January, the businesses that truly succeed are the ones that rely on systems and routines—not guesswork —to manage their finances. Strong bookkeeping habits create clarity, reduce stress, and support smarter decision-making all year long. Here are the essential financial habits every small business should establish to start the year strong.

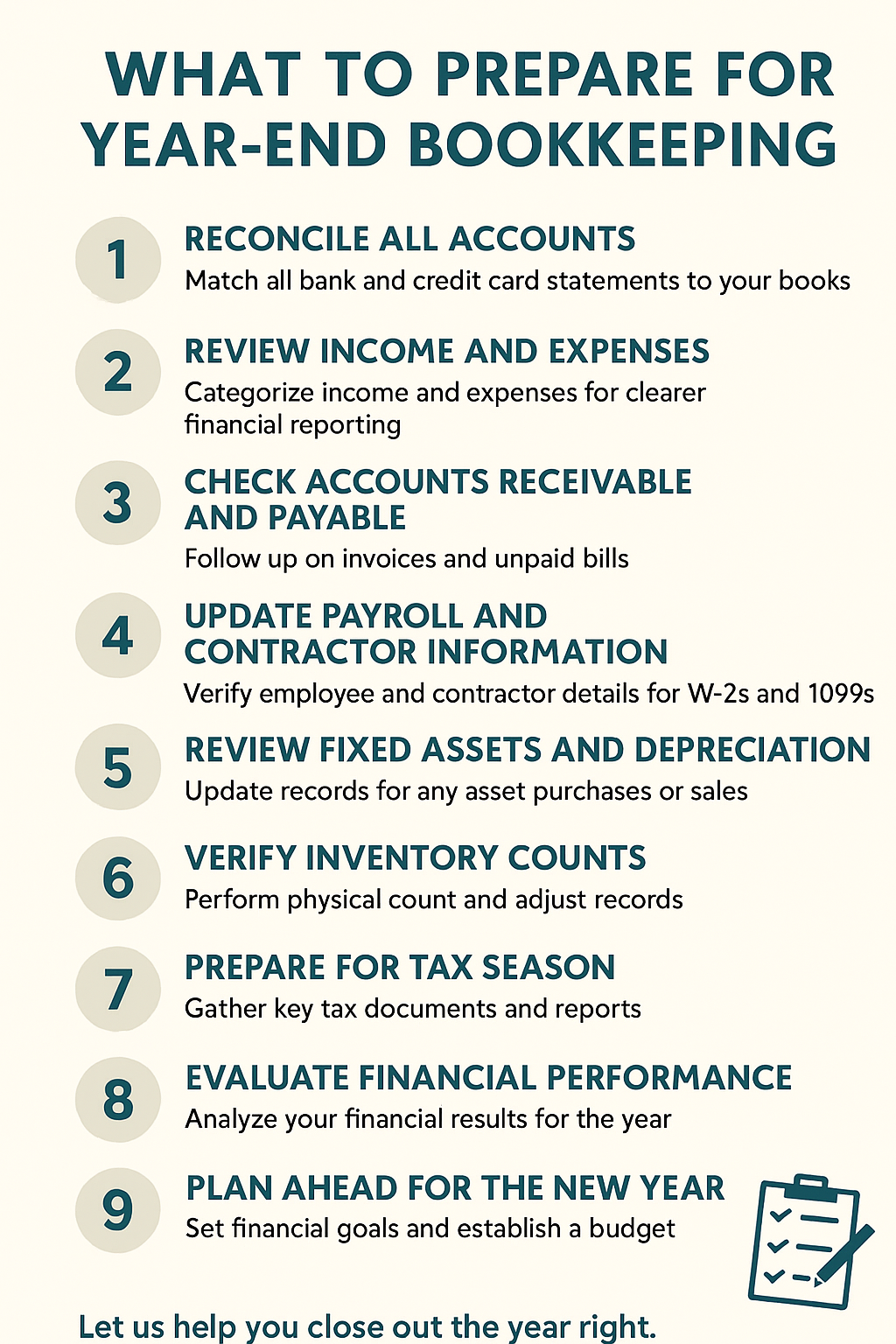

A new year brings new goals, new opportunities, and a fresh chance to move your business forward with confidence. But before you can set smart financial goals for the year ahead, you need a clear picture of where you’ve been—and that’s where bookkeeping plays a vital role. Accurate bookkeeping gives you the financial visibility needed to make informed decisions. Here’s how wrapping up the year properly sets you up for success:

A Practical Guide for Small Business Owners

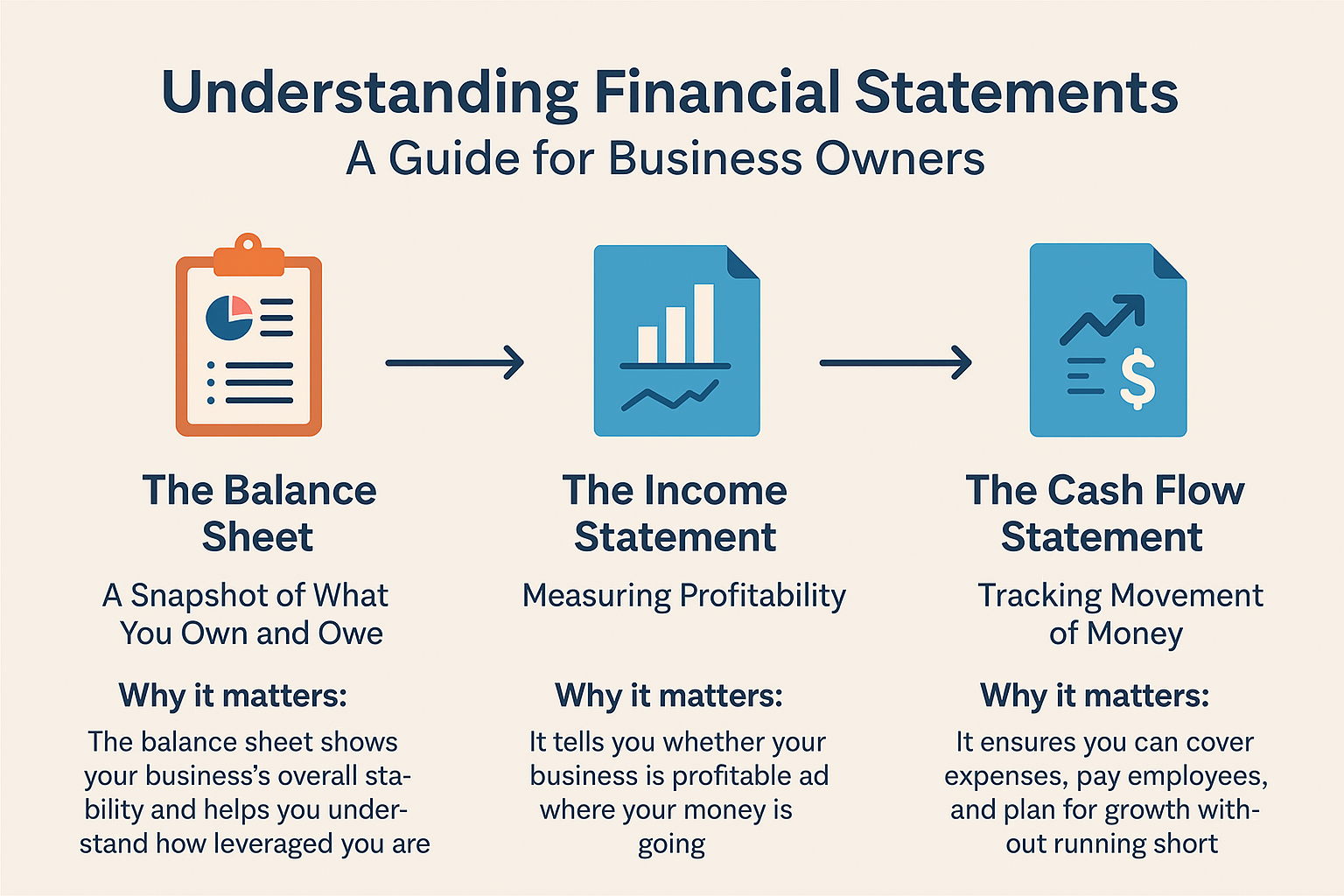

A Guide for Business Owners Financial statements are the roadmap to your business’s financial health. Yet many small business owners see them as a mystery—numbers, charts, and terms that feel more confusing than helpful. The truth is, once you understand what these statements are telling you, they become powerful tools for making better business decisions. At LOV Bookkeeping, we help clients go beyond just “having the books done.” We make sure they understand what their numbers mean. Here’s a simple breakdown of the three key financial statements every business owner should know.

In today’s digital world, small businesses rely heavily on technology to manage finances. While this makes bookkeeping faster and more efficient, it also means sensitive financial data is more vulnerable than ever. A data breach or security lapse can lead to financial loss, compliance issues, and damage to your reputation. At LOV Bookkeeping, we understand how important it is to protect your information. Here are some best practices to keep your financial data safe and secure.