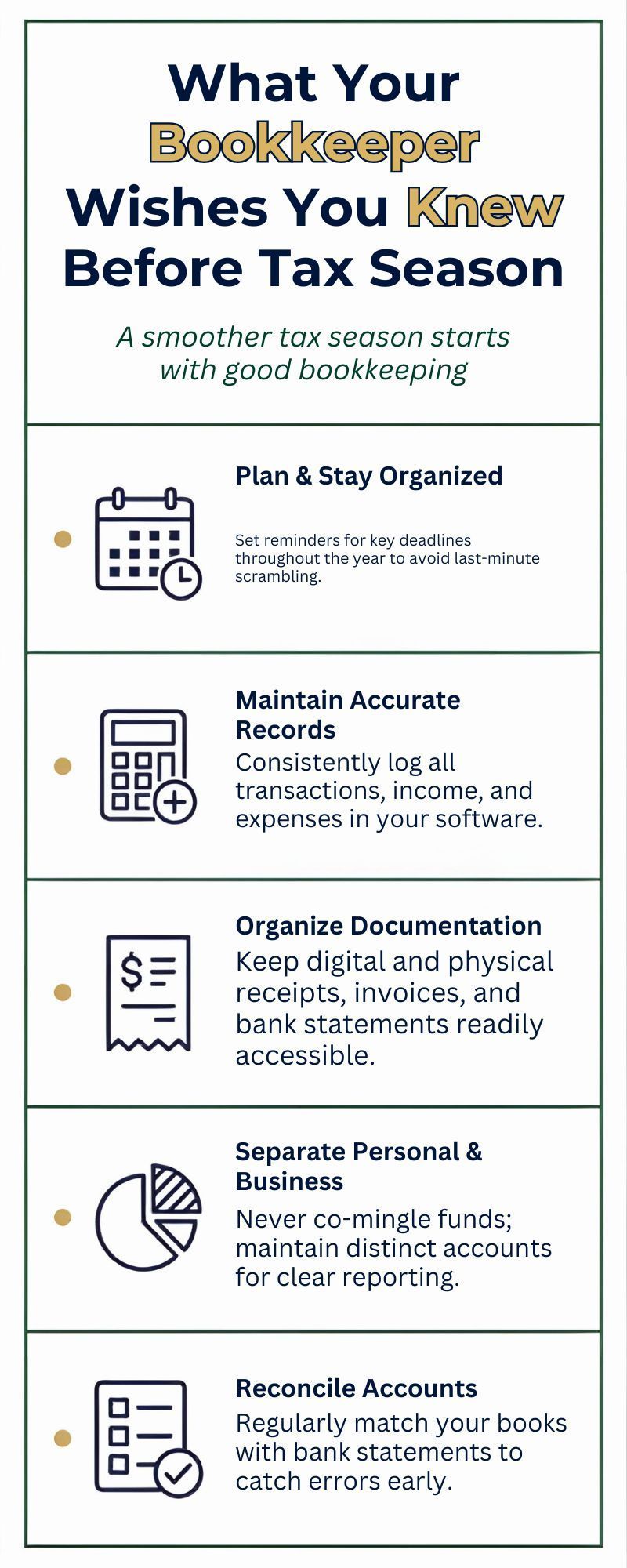

What Your Bookkeeper Wishes You Knew Before Tax Season

For many small business owners, tax season feels stressful, confusing, and rushed. Documents are being gathered at the last minute, questions pop up unexpectedly, and everyone is trying to meet deadlines.

But the truth is, tax season doesn’t have to feel that way.

A lot of the stress that happens in March and April could be avoided with better bookkeeping habits throughout the year. As bookkeepers, we see the same patterns every year, and there are a few things we wish every business owner understood before tax season arrives.

Your Books Should Already Be Done

One of the biggest misconceptions about tax season is that it’s the time when the books finally get organized.

In reality, by the time tax preparation begins, your books should already be clean, reconciled, and finalized for the year. When bookkeeping is kept up monthly, tax season becomes much simpler. Instead of scrambling to reconstruct the year, your accountant can focus on preparing accurate returns and identifying tax-saving opportunities.

Good Bookkeeping Saves You Money

Many business owners think bookkeeping is just about staying organized. In reality, good bookkeeping can directly impact how much you pay in taxes.

Accurate records ensure that all legitimate business expenses are captured and categorized correctly. When your books are messy or incomplete, deductions can easily be missed.

Clean books also allow your accountant to work more efficiently, which can reduce the time and cost involved in preparing your return.

Separation Between Business and Personal Matters

Another issue that creates problems at tax time is mixing personal and business transactions.

Using the same accounts or credit cards for both can complicate bookkeeping and create unnecessary questions during tax preparation. Keeping your finances separate makes everything easier to track, categorize, and verify.

It’s one of the simplest habits that can dramatically improve financial clarity.

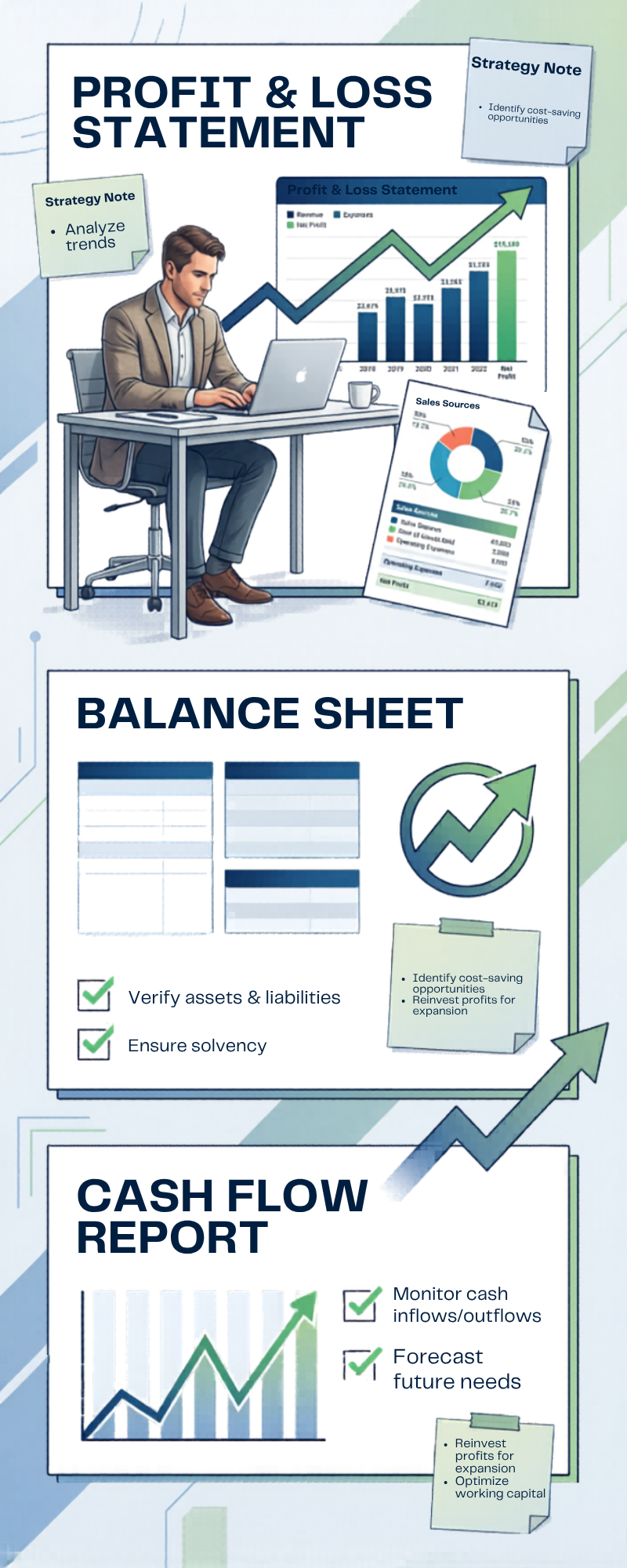

Your Financial Reports Tell a Story

Your bookkeeping isn’t just for tax filing. It also tells the story of how your business performed throughout the year.

Your Profit and Loss Statement shows whether your business was profitable. Your Balance Sheet shows what your business owns and owes. When these reports are accurate and updated regularly, they become powerful tools for making better decisions.

Tax season simply becomes the final chapter in that story.

The Best Tax Seasons Start Months Earlier

The smoothest tax seasons happen when bookkeeping is done consistently throughout the year. Monthly reconciliation, organized records, and accurate categorization mean there are no surprises when it’s time to file.

Instead of stress and confusion, business owners can move through tax season with confidence.

How LOV Bookkeeping Helps

At LOV Bookkeeping, our goal is to make tax season easier for both you and your accountant. By maintaining clean, accurate books all year long, we help ensure that when tax season arrives, everything is already prepared.

That means fewer surprises, clearer financial insight, and more time for you to focus on running your business.

Because when your books are in order, tax season becomes a process—not a panic.