As the end of the year approaches, small business owners have more than holiday sales and schedules on their minds. It’s also time to get the books in order. Year-end bookkeeping isn’t just about closing the books — it’s about setting your business up for a strong start in the new year.

Here’s a practical checklist to help you prepare for year-end bookkeeping and avoid last-minute stress.

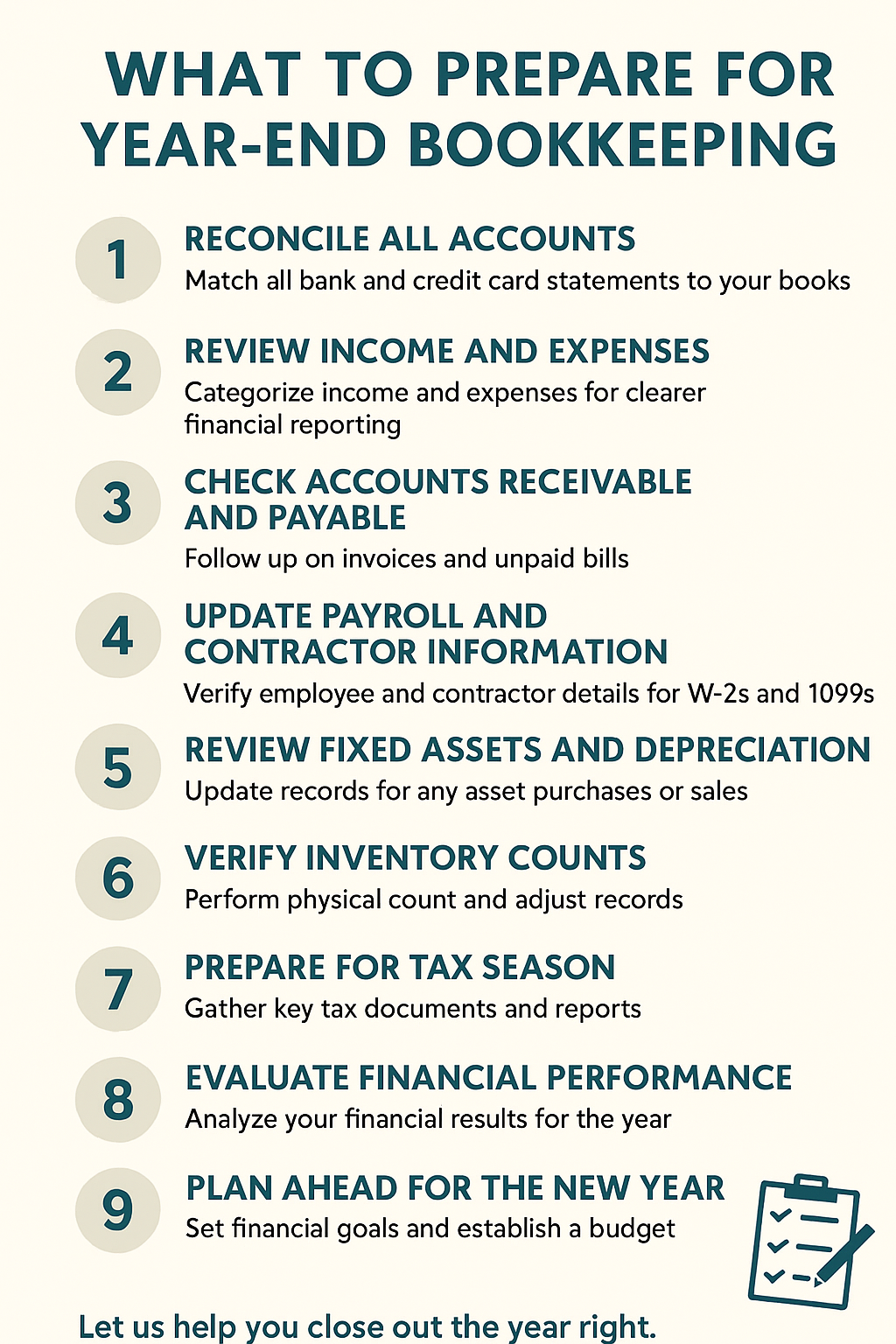

1. Reconcile All Accounts

Make sure your bank accounts, credit cards, and loans match the balances on your statements. Reconciling ensures every transaction is recorded properly and helps identify missing entries or duplicate expenses. It’s one of the simplest — but most crucial — steps in ensuring your books are accurate.

2. Review Income and Expenses

Take time to categorize all income and expenses correctly. This step is key for:

Understanding your business’s profitability

Identifying deductible expenses

Avoiding surprises when tax time rolls around

If you’ve been using general categories or “miscellaneous” labels, now’s the time to clean those up for a clearer financial picture.

3. Check Accounts Receivable and Payable

Follow up on outstanding invoices and unpaid bills. Collecting what’s owed and paying what you owe keeps your financial reports clean and helps improve your cash flow. It’s also a good time to evaluate if your payment terms need adjusting for next year.

4. Update Payroll and Contractor Information

Ensure all employee and contractor information is current and accurate. You’ll need correct addresses and tax details for W-2s and 1099s. Review any bonuses, reimbursements, or benefits to confirm they’ve been properly recorded.

5. Review Fixed Assets and Depreciation

If you purchased or sold equipment, vehicles, or property this year, update your fixed asset list (yes, you should have a list). Properly tracking these ensures your depreciation is recorded correctly — which can significantly affect your tax deductions.

6. Verify Inventory Counts

For businesses that carry inventory, do a physical count and compare it to what’s in your system. Adjust for shrinkage, spoilage, or discrepancies. Accurate inventory counts directly impact your cost of goods sold and your bottom line.

7. Prepare for Tax Season

Gather key tax documents and reports now, such as:

- Profit & Loss Statement

- Balance Sheet

- General Ledger

- Payroll Reports

- Receipts for major purchases or deductions

- Having these ready makes tax filing faster — and can reduce the stress that comes with deadlines.

8. Evaluate Financial Performance

Once your books are up-to-date, step back and analyze your numbers. How did your revenue compare to last year? Which expenses grew, and why? This is your chance to identify what’s working and what needs adjustment before the new year begins.

9. Plan Ahead for the New Year

Finally, use this momentum to set financial goals. Whether it’s improving cash flow, increasing profit margins, or simply keeping more organized books — start planning now. A clean close this year sets the foundation for smoother, more informed decisions next year.

Need Help Closing Out the Year?

Year-end bookkeeping can be overwhelming, especially when you’re trying to wrap up projects and plan for the holidays. At LOV Bookkeeping, we help small business owners close their books accurately and efficiently — so you can focus on growth, not paperwork.

Let’s make sure your year ends right.

Book a no obligation consultation with us today.