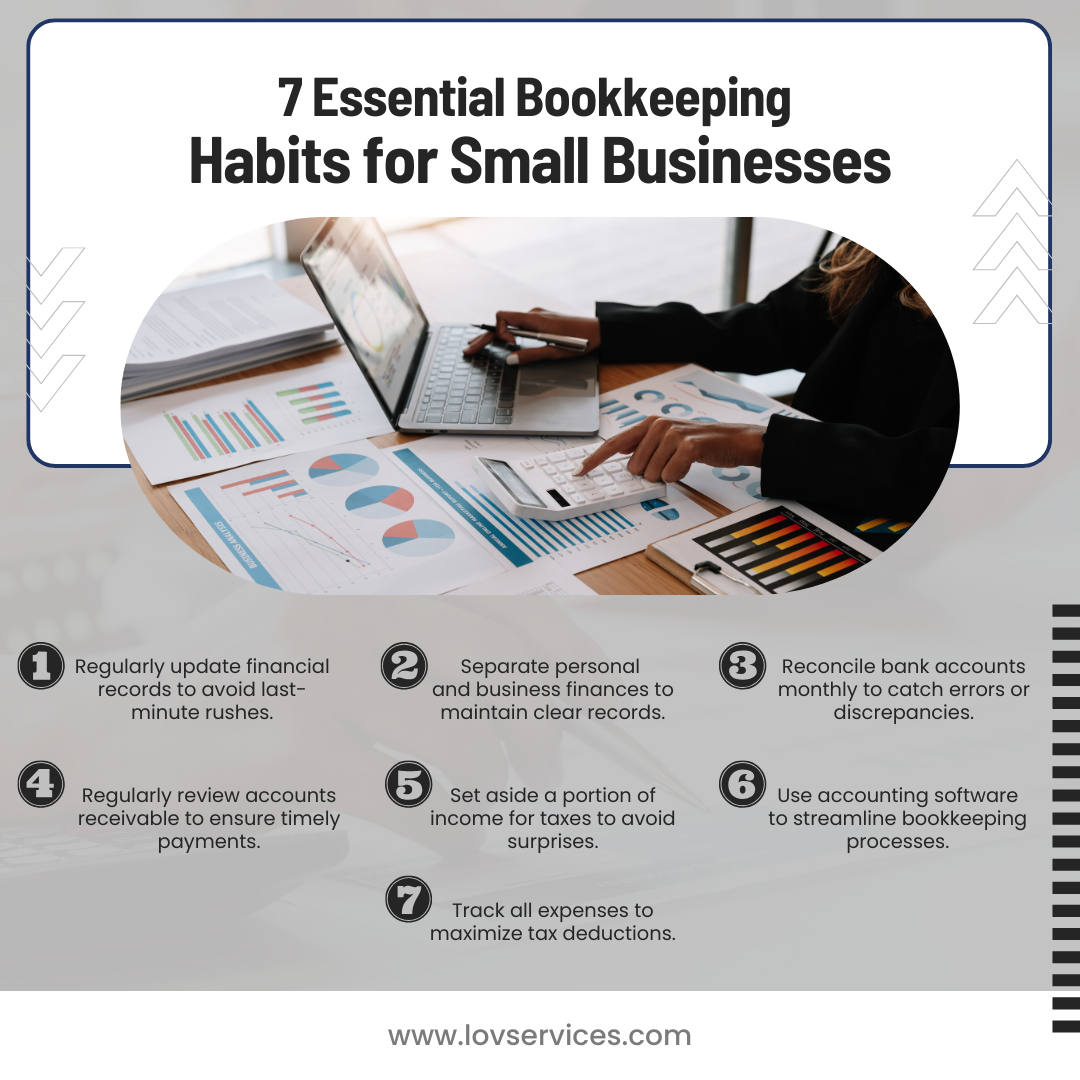

7 Bookkeeping Habits for Small Businesses

July 22, 2024

Maintaining accurate and up-to-date bookkeeping is essential for the success of any small business. As a small business owner, it's crucial to develop good bookkeeping habits to ensure the financial health of your company. Here are seven essential bookkeeping habits that every small business should adopt:

- Regularly update financial records: Avoid the last-minute rush by making a habit of updating your financial records on a consistent basis, whether it's daily, weekly, or monthly. This will help you stay on top of your finances and make informed decisions.

- Separate personal and business finances: It's important to keep your personal and business finances completely separate. This will make it easier to track expenses, generate accurate financial reports, and ensure compliance with tax regulations.

- Reconcile bank accounts monthly: Make it a habit to reconcile your bank accounts on a monthly basis. This will help you catch any errors or discrepancies early on, preventing larger issues down the line.

- Review accounts receivable regularly: Stay on top of your accounts receivable by reviewing them regularly. This will help you identify any late payments or outstanding invoices, allowing you to take prompt action to collect the owed funds.

- Set aside a portion of income for taxes to avoid surprises. Similar to having an emergency fund, this will help you to make sure you can cover your tax payments without having to resort to borrowing.

- Use accounting software to streamline bookkeeping processes. If you’re small enough, you may be able to do your books on excel or with receipts, but most small businesses should have accounting software that matches their needs.

- Track all expenses to maximize tax deductions. If you’re already practicing habits 1 thru 6, this should be happening. However, it’s worth a special mention here!

By adopting these seven bookkeeping habits, you'll be well on your way to maintaining a strong financial foundation for your small business, allowing you to focus on growth and success. At LOV bookkeeping, we work with small business owners to make sure they have these processes in place and they are being followed. We can take care of the heavy lifting here while you focus on doing the things that help grow your business.

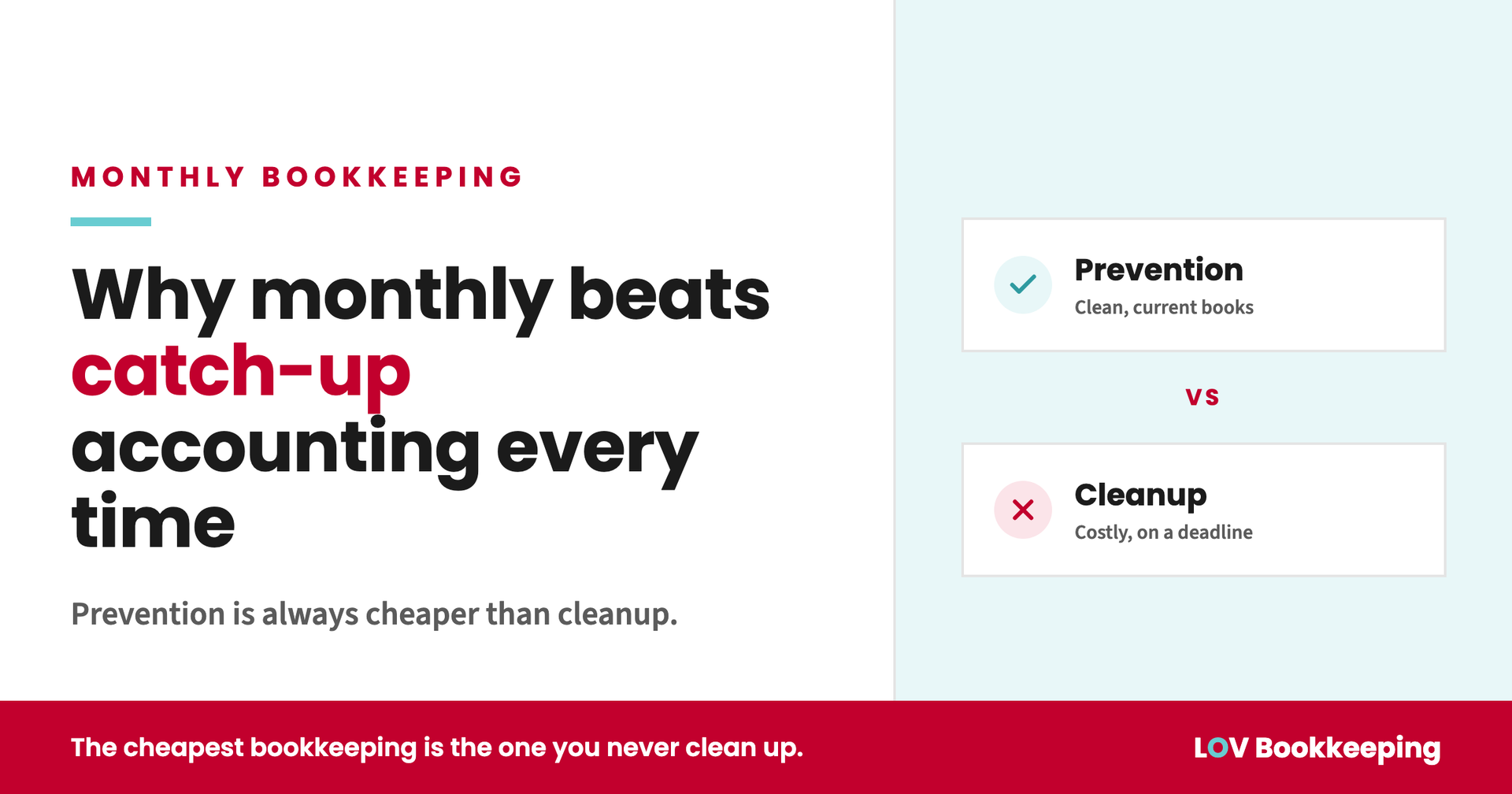

Most business owners we talk to assume catch-up bookkeeping is the budget-friendly choice. Let the books sit, hand off a pile of statements once or twice a year, and pay for a single cleanup instead of an ongoing service. On paper that sounds reasonable. In practice it usually costs more.

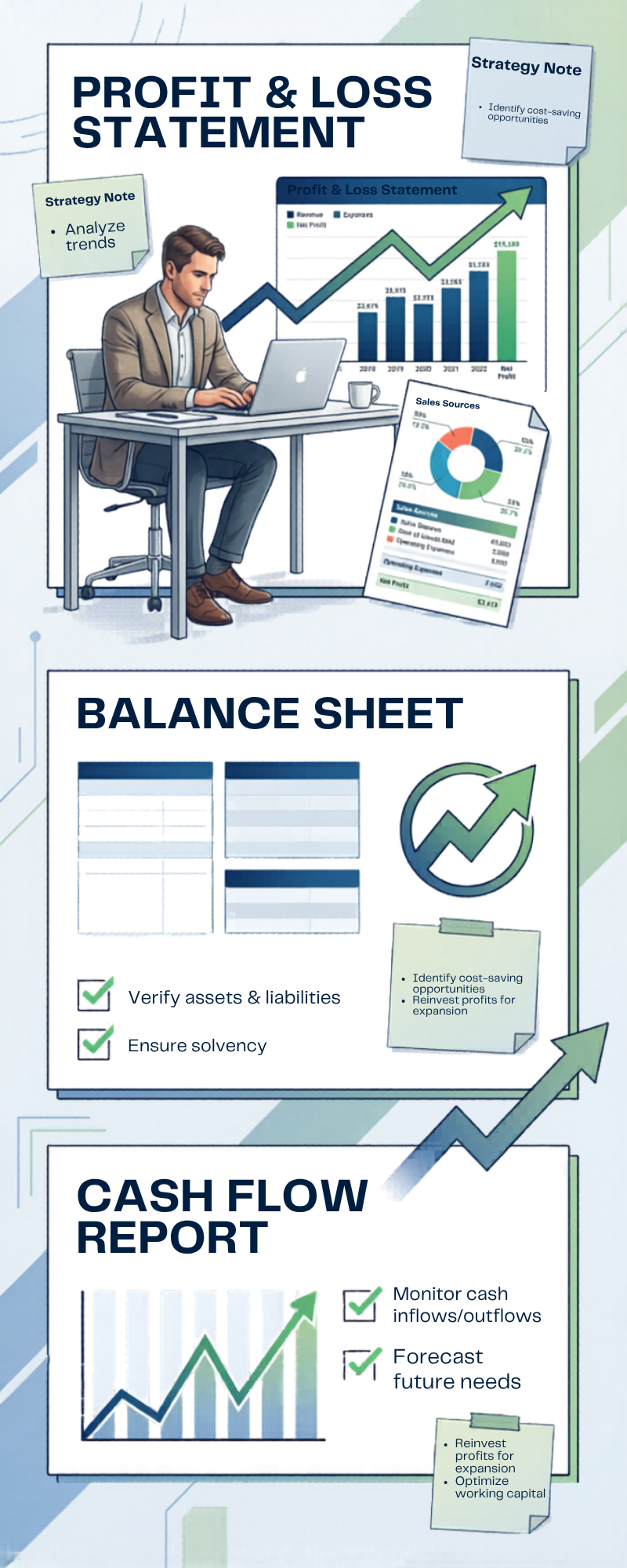

Many small business owners receive financial reports every month… but never really use them. The reports get downloaded, glanced at briefly, and filed away until tax season. But financial reports are much more than paperwork—they’re decision-making tools. When you understand what your numbers are telling you, you can make smarter, more confident choices for your business. Here’s how to turn your financial reports into actionable insights. Your Profit & Loss Statement Shows What’s Working Your Profit & Loss Statement (P&L) tracks: Revenue Expenses Profitability This report helps answer important questions like: Are you actually making money? Which services or products are most profitable? Are expenses increasing too quickly? Reviewing your P&L monthly helps you spot trends early instead of reacting after problems grow. Your Balance Sheet Reveals Financial Stability Your Balance Sheet gives you a snapshot of: What your business owns (assets) What it owes (liabilities) Your equity position This report helps you understand the overall financial health of your business. For example: Too much debt may signal risk Strong cash reserves create flexibility Growing assets often indicate stability and growth Cash Flow Tells You Whether Your Business Can Breathe Profit does not always equal cash in the bank. Your cash flow shows: Money coming in Money going out Whether you can comfortably cover expenses Many profitable businesses still struggle because they don’t monitor cash flow carefully. Understanding this report helps you avoid surprises and plan ahead with confidence. Financial Reports Help You Make Smarter Decisions When your reports are accurate and up to date, they help guide decisions like: Hiring employees Increasing prices Cutting unnecessary expenses Expanding services Investing in equipment or marketing Instead of relying on guesswork or emotions, you’re making decisions based on real data. Consistency Creates Clarity Financial reports only become useful when they’re reviewed consistently. Monthly bookkeeping and regular financial reviews allow you to: Spot problems early Track progress toward goals Make adjustments quickly Good financial habits lead to better long-term business decisions. How LOV Bookkeeping Helps At LOV Bookkeeping, we believe bookkeeping is about more than recording transactions. We help small business owners: Understand their financial reports Identify trends and opportunities Gain clarity about their business performance Make informed, confident decisions Because when you understand your numbers, you can lead your business with confidence.

For many small business owners, doing your own bookkeeping feels like the responsible thing to do. It saves money, keeps you in control, and seems manageable, at least at first. But what most business owners don’t realize is that DIY bookkeeping often comes with hidden costs. Over time, those costs can add up to far more than hiring a professional. Let’s take a closer look at the real cost of doing your own books.